If you work in mortgage lending or AMC operations, you’ve felt the friction.

A lender submits an appraisal order. The AMC receives it, manually routes it to an appraiser, waits for confirmation, sends a status update, and waits again. Somewhere in that chain, a deadline slips, a document goes missing, or a compliance checkbox doesn’t get checked. The loan officer calls. The processor follows up. The borrower gets frustrated.

This isn’t a problem for people. It’s an infrastructure problem.

Appraisal management software exists specifically to eliminate this friction, and when it’s implemented well, the improvement in speed, accuracy, and compliance is substantial. Here’s how it closes the five most costly gaps between AMCs and the lenders they serve.

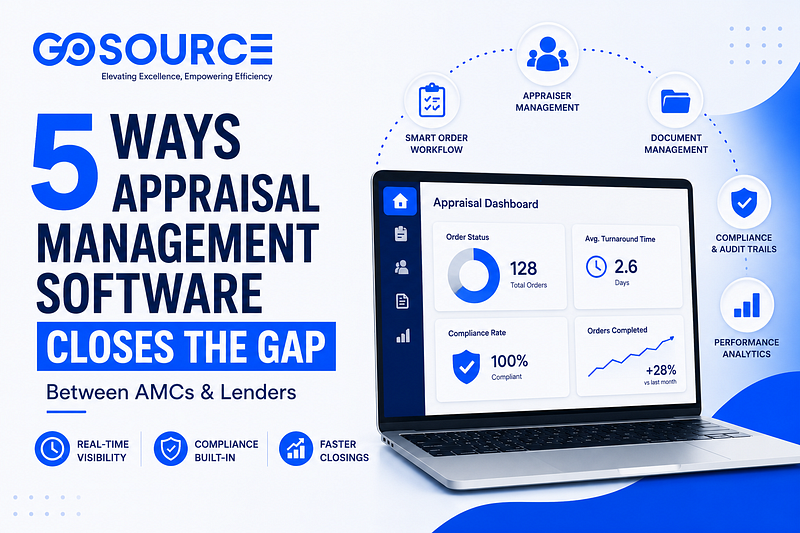

1. It replaces status uncertainty with real-time visibility

The single most common frustration between AMCs and lenders isn’t quality; it’s communication. Specifically, the lack of it at critical moments: when an order is accepted, when an inspection is scheduled, when a report is ready for review.

Manual workflows rely on people remembering to send updates. That works until volume spikes, or someone is out of the office.

Appraisal management software automates status updates at every stage of the order lifecycle. Lenders get notified when orders are placed, assigned, inspected, and completed without having to chase anyone. AMCs spend less time fielding status inquiry calls and more time on work that actually requires human judgment.

The result: both sides operate from the same real-time picture.

2. It builds compliance into the workflow rather than bolting it on after the fact

Appraisal independence requirements under Dodd-Frank are non-negotiable. USPAP governs how appraisals are conducted and reviewed. GSE guidelines set documentation standards for loans that need to be sold into the secondary market.

Meeting these requirements manually means relying on people to follow the process every time, without exception. That’s a fragile system.

Appraisal management software makes compliance structural. Access controls prevent loan production staff from influencing appraiser selection. Audit logs record every action taken on every order. Review checklists are embedded in the workflow, not attached as a reminder email.

When an audit happens, and it will, the documentation exists automatically. This is the difference between a compliant shop and a defensible one.

For a detailed breakdown of how compliance-ready appraisal workflows are structured, GoSource Valuation’s appraisal management software page covers the architecture well.

3. It turns appraiser panel management from reactive to strategic

Most AMCs have a panel of appraisers they rely on. Managing that panel manually, tracking credentials, license renewals, geographic coverage, performance history, and current capacity is an enormous operational burden.

Appraisal management software centralizes all of this in a searchable database. When an order comes in, the system identifies qualified appraisers for that geography, checks current capacity, and facilitates assignment either automatically or with human oversight.

Over time, the performance data generated by the system, including turnaround times, revision rates, and client feedback, creates an objective foundation for panel management decisions. The AMC can identify which appraisers are consistently reliable, and which are creating friction and manage the panel accordingly.

This is closely related to what Go Source covers in the appraiser scorecard methodology a structured approach to evaluating and managing appraiser performance at scale.

4. It eliminates the document management problem at the root

Appraisal operations generate a significant volume of documents: orders, reports, revision requests, inspection photos, correspondence, and invoices. In a manual environment, these documents live in email inboxes, shared drives, and, let’s be honest, someone’s desktop.

Finding a specific document when it’s needed is frustrating. Finding it during a compliance review is stressful. Not finding it at all has real consequences.

Appraisal management software stores all documents digitally, linked to the corresponding order record. Version control tracks revisions. Retrieval is fast and searchable. Nothing lives in a personal email.

For AMCs handling hundreds or thousands of orders per month, this isn’t a marginal improvement; it’s a fundamental change in operational reliability.

5. It gives both sides the analytics to improve

Here’s something manual workflows can’t do tell you where your process is breaking down.

How long does it take for your team to assign an order after receipt? What’s the average time from inspection to report delivery? Which appraisers are running above average revision rates? What’s your compliance exception rate over the last quarter?

Without software, answering these questions requires someone to manually pull data from multiple systems and build a spreadsheet. It happens quarterly if at all, and by the time the analysis is done, the operational moment has passed.

Appraisal management software surfaces this data continuously. AMC managers and lender operations teams can see trends in real time and adjust before small problems compound into costly ones.

For lenders and AMCs thinking about how performance data connects to broader quality control strategy, the GoSource Valuation blog has solid coverage of appraisal QC practices worth bookmarking.

FAQ: Appraisal Management Software for AMCs and Lenders

What’s the core difference between appraisal management software designed for AMCs versus lenders?

AMC-focused platforms tend to emphasize appraiser panel management, order routing, and vendor compliance. Lender-focused tools often prioritize LOS integration, borrower communication, and audit trail documentation. The best platforms serve both needs.

Does appraisal management software replace the need for AMC services?

Not necessarily. Software handles operational infrastructure workflow, documentation, and compliance tracking. AMCs provide the human judgment layer: appraiser relationships, escalation handling, quality review, and client communication. Many lenders use both.

How does this software handle the shift to hybrid and desktop appraisals?

Modern platforms are built to accommodate multiple appraisal types, including hybrid and desktop formats, gaining traction under UAD 3.6. Order management workflows and document storage adapt to the specific form type and inspection methodology.

Can smaller AMCs realistically implement appraisal management software?

Yes. In fact, smaller AMCs often see the largest proportional benefit because they’re typically running on leaner staffing. The automation gains from software are most impactful when the alternative is a single person managing everything manually.

What should an AMC look for in a software vendor?

Compliance architecture, appraiser panel flexibility, LOS integration capability, reporting depth, and critically, the support model. In high-volume operational environments, vendor responsiveness matters as much as feature set.

Is there a managed service option for AMCs that want operational support alongside software?

Yes. Some firms offer AMC operations services that combine software infrastructure with staffed support for order management, QC, and appraiser coordination. Go Source Valuations AMC operations solutions are one example of this model.

Final Thought

The friction between AMCs and lenders in the appraisal process isn’t inevitable; it’s structural. And most of it traces back to the same root cause: information and documents moving through manual channels that weren’t designed for the volume, compliance demands, or turnaround expectations of today’s lending environment.

Appraisal management software solves that at the infrastructure level. The AMCs and lenders who adopt it don’t just run cleaner operations; they’re better positioned for the scrutiny that comes with regulatory examinations, GSE audits, and borrower complaints.

The right technology, deployed with the right operational support, is what separates reactive appraisal teams from consistently high-performing ones.